Esperamos a asegurarnos de que estuvieras interesado en el contenido de este sitio web antes de molestarte, pero nos encantaría ser tus compañeros durante tu visita...

June 16, 2026

Flex-living has gone from niche terminology to the fastest-growing segment in Spanish real estate investment. In 2025, it attracted €790 million — four times more than in 2023 — and in the first quarter of 2026, the broader living sector surpassed €2.3 billion, up 98% year-over-year. This isn't a trend: it's a structural reset of the residential market, and investors who are recognizing it early are capturing net yields that traditional rentals can no longer offer.

This guide explains exactly what flex-living is, what real returns you can expect, the risks nobody talks about, and how managed investment works for those who want exposure to the sector without becoming an operator.

Flex-living is residential accommodation with contracts ranging from one to eleven months, fully furnished and move-in ready, with a service layer — utilities, wifi, cleaning, maintenance, incident management — professionally operated through a digital platform.

It is not vacation rental. The difference isn't just semantic: vacation rentals operate under tourist apartment licenses, depend on seasonal demand, and face mounting regulatory pressure in every major Spanish city. Flex-living operates under fixed-term tenancy agreements governed by Spain's Urban Leasing Act (LAU), with minimum stays of one month and demand driven by labor mobility, academic relocation, and international professionals — not tourism.

The typical tenant is not a tourist. They're an international master's student, a corporate professional on assignment, a digital nomad looking for a three-month base, or an executive in the middle of a relocation. This profile pays more than a traditional tenant, stays longer than a tourist, and generates less operational friction than either.

Three vectors are converging right now — and not by coincidence.

Demand is structural, not cyclical. Spain received over 240,000 international students in the 2025/26 academic year and ranks among the top three destinations worldwide for digital nomads. This demand doesn't fluctuate with the domestic economic cycle: when the local market cools, international demand stays.

Regulation has squeezed competing supply. Spain's Housing Act (Ley 12/2023) and the Residential Rent Reference Index (IRAV) have capped rents in stressed market zones. The result has not been more traditional rental supply — it's been less. Landlords are pulling properties from the market because the return no longer justifies the risk of an indefinite lease. That stock migrates toward mid-term rentals, but professionally managed flex-living supply remains scarce outside Madrid and Barcelona. In Valencia, Málaga, and Bilbao, demand exists and managed inventory is almost nonexistent.

The yield gap is gaining relative value. With the ECB ruling out further rate cuts and markets pricing in hikes toward 2.5–2.75% through 2026–2027, the cost of financing has stopped falling. In that environment, an asset that defends a 6–6.5% net yield against the 4–4.5% of traditional rentals gains significant relative appeal for any investor comparing real-return alternatives.

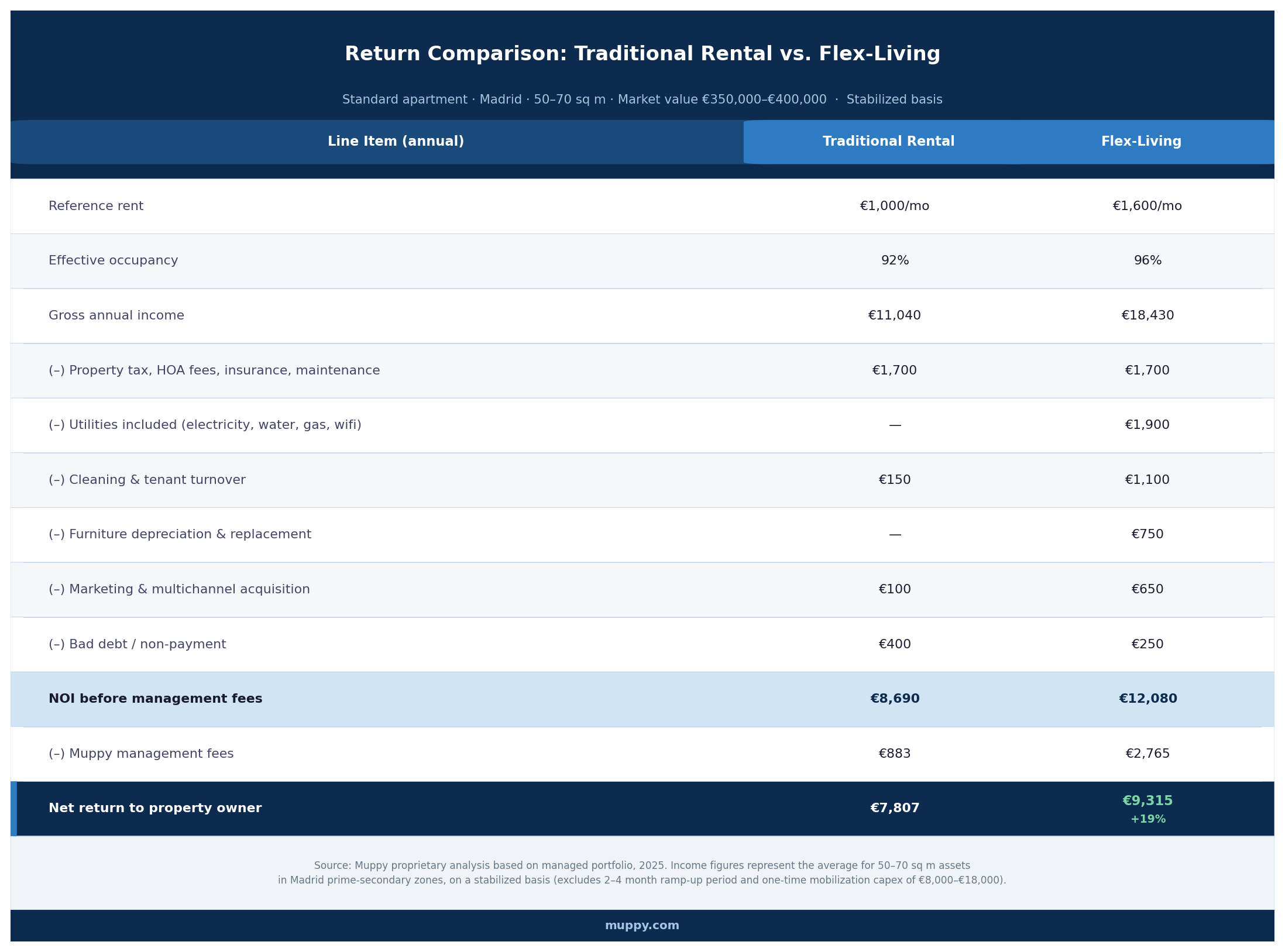

The honest comparison is always net, never gross. Flex-living costs more to operate than traditional rentals — utilities, cleaning, tenant turnover, marketing, furniture replacement — and that higher opex has to be in the equation from day one.

For a standard apartment in Madrid, 50–70 sq m, with a market value of approximately €350,000–€400,000, the stabilized figures look like this:

The net result rises 19% on the same asset — and that jump comes from revenue (higher ARPU, higher occupancy), not from cutting costs. Net yield on market value lands at 6–6.5%, versus 4–4.5% for conventional rental.

Two details to understand before running your own numbers. First, the ramp-up period: for the first 2–4 months after onboarding, income runs below stabilized levels while target occupancy is reached. Second, mobilization capex: furnishing and equipping a property for flex-living requires a one-time investment of €8,000–€18,000 depending on the asset's condition — this doesn't appear in the annual operating statement but does affect total return on investment.

To calculate the specific return for your property using real parameters — acquisition price, location, asset type — use our real estate investment calculator.

Flex-living has risks. Ignoring them is the most common mistake made by investors drawn in purely by the yield.

Contractual risk. A fixed-term tenancy agreement is only valid when a real, documented purpose exists — studies, temporary work, training — and the tenant has their primary residence resolved elsewhere. A poorly structured contract can be reclassified by a court as an indefinite lease, at which point the landlord inherits the full tenant protections they thought they had avoided. This is the most underestimated risk in the sector, and the clearest differentiator between a rigorous operator and one who simply furnishes apartments.

Operational risk. The 96% occupancy shown in the table doesn't happen on its own. It requires continuous marketing, dynamic pricing, fast tenant turnover management, and acquisition channels — corporate, university partnerships, specialized platforms — that individual landlords neither have nor can build efficiently.

Regulatory risk. Spain's rental regulation is still evolving. What currently operates under fixed-term tenancy agreements could be affected by new regional or municipal restrictions. Investors who diversify across cities and operate with strict legal compliance are far better positioned to weather this risk than those concentrated in a single market.

Muppy's model is built for investors who want exposure to flex-living without taking on the operational complexity. It works as a fully delegated management platform: the investor provides the asset — whether an existing property in their portfolio or a new acquisition — and Muppy handles everything else.

That includes multichannel marketing, properly structured and documented fixed-term tenancy agreements, dynamic revenue management, day-to-day operations — check-in, check-out, cleaning, maintenance, 24/7 incident response — and real-time reporting on income, occupancy, and KPIs at the standard institutional investors require.

Fees are transparent and aligned with performance: 8% for long-term stays, 15% for mid-term stays — the core flex-living range — and 19% for short-term stays requiring near-daily rotation and revenue management. Investors pay more only when the operation works harder, and in return they earn more.

The result, as the financial analysis shows, is a net return that outperforms traditional rental even after management fees are deducted — with zero operational burden on the property owner.

If you have a residential asset in Spain and want to know what return it could achieve in flex-living, start by running the numbers with your property's actual parameters:

Real estate investment calculator

Investment mortgage calculator

And if you'd like to speak with a specialist about your specific situation, Muppy offers personalized return analyses at no cost or commitment.